Longer Term Short Options Trend Following – Russell 2000 Test Results

General Idea:

A little while ago I mentioned that I was working on and testing a longer term options trend following system called pTheta. Essentially, I wanted to take a step back from the daily market noise and create a simple solution for selling naked options. The pTheta system trades from a weekly chart and uses Parabolic SAR (pSAR) to determine trend. pTheta sells out of the money options in the direction of the trend with the idea that even if the trend fails, price is unlikely to make it to the short option. This system sells naked options every month in several uncorrelated markets.

The following is a discussion of the system and some initial results on the Russell 2000.

System Settings & Rules:

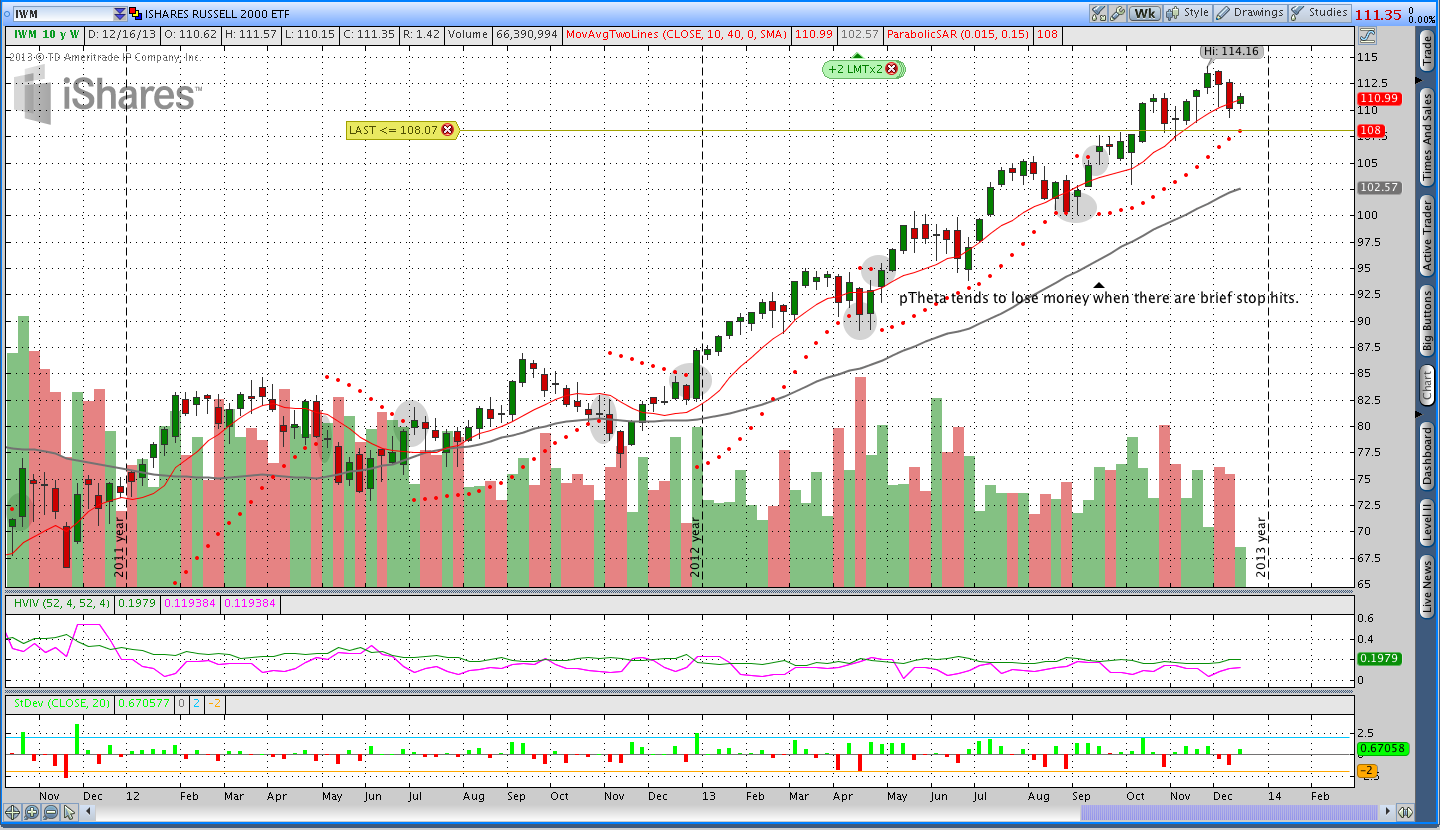

Trend direction is based on a weekly chart with pSAR. The pSAR settings used are an Acceleration Factor = .015 and an Acceleration Limit = .15. pTheta sells out of the money naked options with approximately 90 days to expiration at around a 10 delta. For example, if pSAR is above the market (indicating the system is short) and price hits pSAR to signal a new long trade, the system sells 90 day, 10 delta puts below the market. The system allows the options to expire as long as pSAR is not hit. As a result, the system is always in the market.

Risk Management:

The system sells naked options, however the maximum loss per trade is theoretically limited to the initial credit received (we can’t control gaps). If the open loss on a position is greater than the initial premium, the system closes the trade. In an effort to move out of the way of the market, the system can roll positions when the short delta increases from 10 to 16 or the open loss is equal to 60% of the initial credit. When rolling, the system doubles size and moves both on the options chain and out in time.

Many options traders like to trade nondirectional spreads or naked options and roll the positions as an immediate defense when price moves against the position. The idea behind pTheta is that we’re generally staying on the right side of the market, which minimizes the need to roll.

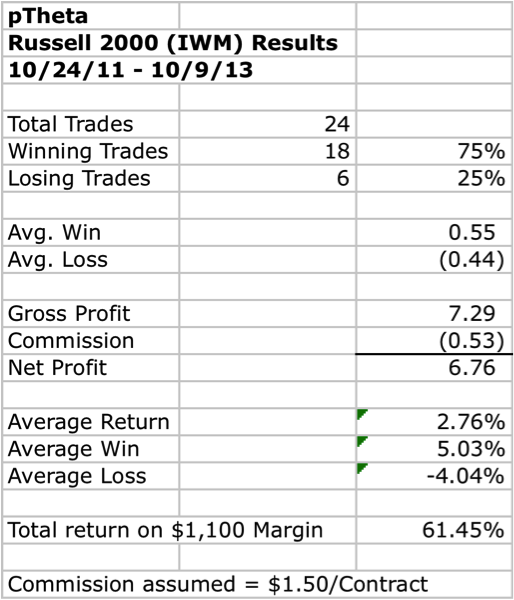

Russell 2000 Results:

The Russell 2000 results below do not include the rolling rules above. Over the course of 2 years, the rolling rules were only met a couple of times and the impact on the results below was minimal and slightly positive. For simplicity and due to the lack of trades, the rolling results are excluded from the results below.

Margin:

Naked option margin is not a constant number and in this example an average margin estimate was used. Average margin for the purposes of calculating return is based on the current margin. At the time of this writing, a 90 day, 10 delta short put margin for IWM is approximately $1,000 and the 10 delta call is around $1,200. For simplicity, I’m calling average margin $1,100. If you’d like to experiment with margin requirements, there is a cool calculator on the CBOE website.

Test Analysis and Limitations:

The two biggest limitations to the test are that the system only looked back two years and I only tested one market. However, it’s clear from the results that the system does well as long as there aren’t whipsaw reversals in trend. Essentially, the system performed consistently with how we would expect a short gamma trend following system to perform. By and large, the system made more money selling puts both because the premium is richer and trend was generally higher over the 2 years tested.

Looking Ahead:

This is relatively new system and there are quite a few extensions including adding different markets and another trend filter. I’ll be trading the system live in 2014 and posting the results to the blog. I currently have some initial positions open in IWM and GLD. You can check out details about those trades in the Midweek Commentary.

Thanks for reading and please share this post on your preferred social media if you enjoyed it. You can even use that cool hovering toolbar above.

Want to know what’s going on at Theta Trend and see new systems as soon as they’re posted?

Sign up for my email list and stay up to date with the latest happenings.

Click here to get a copy of the Theta Trend Options Trading System, the Trade Tacker I use, and Theta Trend updates.

One thought on “Longer Term Short Options Trend Following – Russell 2000 Test Results”

Comments are closed.